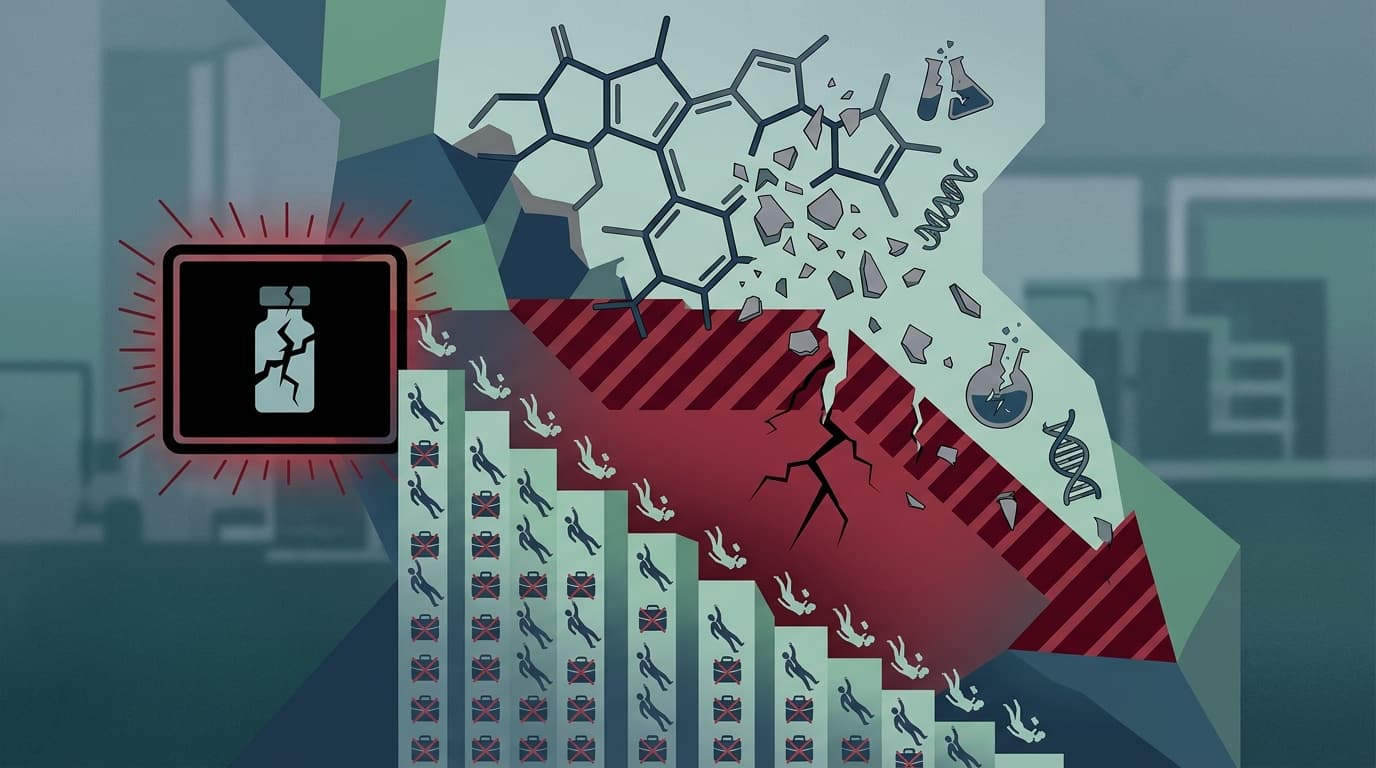

Sarepta's Worst Week: A Black Box Warning and 500 Pink Slips

Sarepta slapped a black box warning on its flagship gene therapy Elevidys after fatal liver failures in young patients, then cut 36% of its workforce in the same breath. The moves signal a company (and an industry) at a crossroads.

Two teenage boys died after receiving a gene therapy that was supposed to save their lives. Now the company behind it is scrambling to survive.

Sarepta Therapeutics just added a black box warning to Elevidys, its flagship gene therapy for Duchenne muscular dystrophy (DMD). That's the FDA's most severe safety label, the regulatory equivalent of a skull and crossbones on a medicine bottle. On the same day, the company announced it's cutting 500 workers, roughly 36% of its entire workforce. For a company that was once the poster child of gene therapy's promise, this is a brutal one-two punch.

The Deaths That Changed Everything

Duchenne muscular dystrophy is a cruel disease. It's a genetic condition that slowly destroys muscle tissue, mostly in boys. Most patients lose the ability to walk by their early teens. Many don't survive past their 20s or 30s. A gene therapy that could halt or slow that progression would be transformative.

Elevidys was supposed to be that therapy. The FDA first approved it in 2023, and Sarepta raced to get it into as many patients as possible. Then came the reports: two non-ambulatory pediatric patients died of acute liver failure after receiving the treatment. A third death was linked to a related therapy using the same viral delivery system (called an AAV vector; think of it as the molecular truck that delivers the therapeutic gene).

The FDA responded with force. The new black box warning highlights the risk of serious liver injury, acute liver failure, and death. The agency also yanked Elevidys's approval for non-ambulatory patients entirely, restricting use to kids who can still walk. Doctors must now run weekly liver function tests for at least three months after infusion. Patients need to stay near a hospital for at least two months post-treatment.

If getting Elevidys used to feel like scheduling a routine (if expensive) procedure, it now feels more like preparing for surgery with a significant complication risk.

Get tomorrow's biotech intelligence before your competitors.

Join thousands of biotech professionals who start their day with our free, daily briefing.

The safety crisis didn't just change the label. It crushed the business.

Sarepta's stock has fallen more than 80% from its highs, recently trading in the $20-40 range after once touching $173 per share. Elevidys revenue, which peaked at $375 million in Q1 2025 alone, slid to just $102 million in the most recent quarter. Doctors are hesitant. Families are scared. The commercial momentum that once seemed unstoppable has stalled.

And there's a ticking clock on the wall: Sarepta has roughly $158.6 million in convertible note debt remaining due in 2027, after exchange transactions extended the bulk of its original obligations to 2030. CEO Doug Ingram acknowledged the stakes directly, saying that failing to adapt would "risk our long-term viability." That's corporate-speak for "we could go under."

The 500 layoffs, combined with pausing several pipeline programs, are expected to save about $400 million per year. That's not a trim; it's an amputation. Sarepta is shutting down most of its limb-girdle muscular dystrophy gene therapy programs and pivoting toward siRNA (a different type of genetic medicine that silences harmful genes rather than replacing them). The company is essentially admitting that its original bet on AAV gene therapy needs a fundamental rethink.

The $500 Million Question

Management has drawn a line in the sand: $500 million in annual Elevidys sales is the minimum needed to keep the lights on and pay down that debt. For 2026, Sarepta is guiding to total revenue of $1.2 to $1.4 billion, a sharp drop from the $2.9 to $3.1 billion it originally projected for 2025.

Wall Street's reaction has been complicated. On one hand, investors were relieved the FDA didn't pull Elevidys off the market entirely. The stock actually popped 20-40% intraday on the restructuring news, because at least there was a plan. On the other hand, the analyst consensus is cautious: price targets range from as low as $5 to a high of around $80 per share, a spread wide enough to drive a truck through. Nobody really knows where Elevidys revenue stabilizes.

The quarterly numbers tell the story of a drug losing altitude. From $375 million in Q1 2025 to $132 million in Q3, then $110 million in Q4, and now $102 million. Each quarter brings new questions about whether demand has bottomed or still has further to fall.

Gene Therapy's Growing Pains

Sarepta's troubles aren't happening in isolation. The entire AAV gene therapy field is dealing with a credibility problem.

Pfizer already abandoned its own DMD gene therapy after a Phase 3 failure and a patient death from cardiac arrest. In 2024, the FDA slapped black box warnings on all six approved CAR-T therapies (a different type of gene-modified treatment) for secondary cancer risk. Earlier in 2026, Regenxbio saw its pediatric AAV program put on clinical hold after a five-year-old developed a brain tumor potentially linked to vector integration, four years after treatment.

The pattern is clear: the FDA's tolerance for gene therapy side effects is shrinking. The agency even revoked Sarepta's "platform technology" designation for its AAVrh74 vector, meaning it can no longer assume that safety data from one program applies to others using the same delivery system. Each drug now has to prove its safety from scratch.

For patients and families hoping gene therapy would be a one-and-done cure, this is sobering. The promise isn't dead, but the fine print just got a lot longer.

Who Fills the Void?

The competitive landscape is shifting fast. Solid Biosciences has its next-generation gene therapy SGT-003 in a Phase 3 trial, designed to address the exact safety and immunogenicity problems that plagued first-generation treatments like Elevidys. Regenxbio's RGX-202 is also in pivotal trials, with a potential FDA filing expected around mid-2026.

But the real threat to Sarepta might not come from another gene therapy at all. Dyne Therapeutics earned an FDA Breakthrough Therapy Designation for DYNE-251, an advanced exon-skipping drug that doesn't require a viral vector. It showed sustained improvements over 18 months in trials, and a filing is expected in early 2026. For families weighing a one-time gene therapy infusion that carries a black box warning against a repeat-dose drug with a cleaner safety profile, the calculus just changed dramatically.

What Comes Next

Sarepta isn't dead. It still has approximately $748 million in cash as of the end of Q1 2026, a portfolio of approved exon-skipping drugs generating over $900 million annually, and a new strategic direction built around siRNA technology. The restructuring, painful as it is, gives the company a plausible path to meeting its debt obligations.

But the broader lesson is hard to ignore. Gene therapy was sold as medicine's moonshot: one infusion, problem solved. Reality has been messier, more dangerous, and far more expensive than anyone predicted. Sarepta's black box warning isn't just a label change. It's a reality check for an entire field that's still learning how to deliver on its biggest promise without hurting the people it's trying to save.

Clinical & Regulatory

5 min read

Lilly's Quiet Move to Win the GLP-1 Price War

Eli Lilly just made every dose of Zepbound available for $499 or less per month, completing a pricing strategy that's quietly reshaping the GLP-1 obesity market. The move intensifies a price war with Novo Nordisk while exposing just how broken insurance coverage for weight-loss drugs remains.