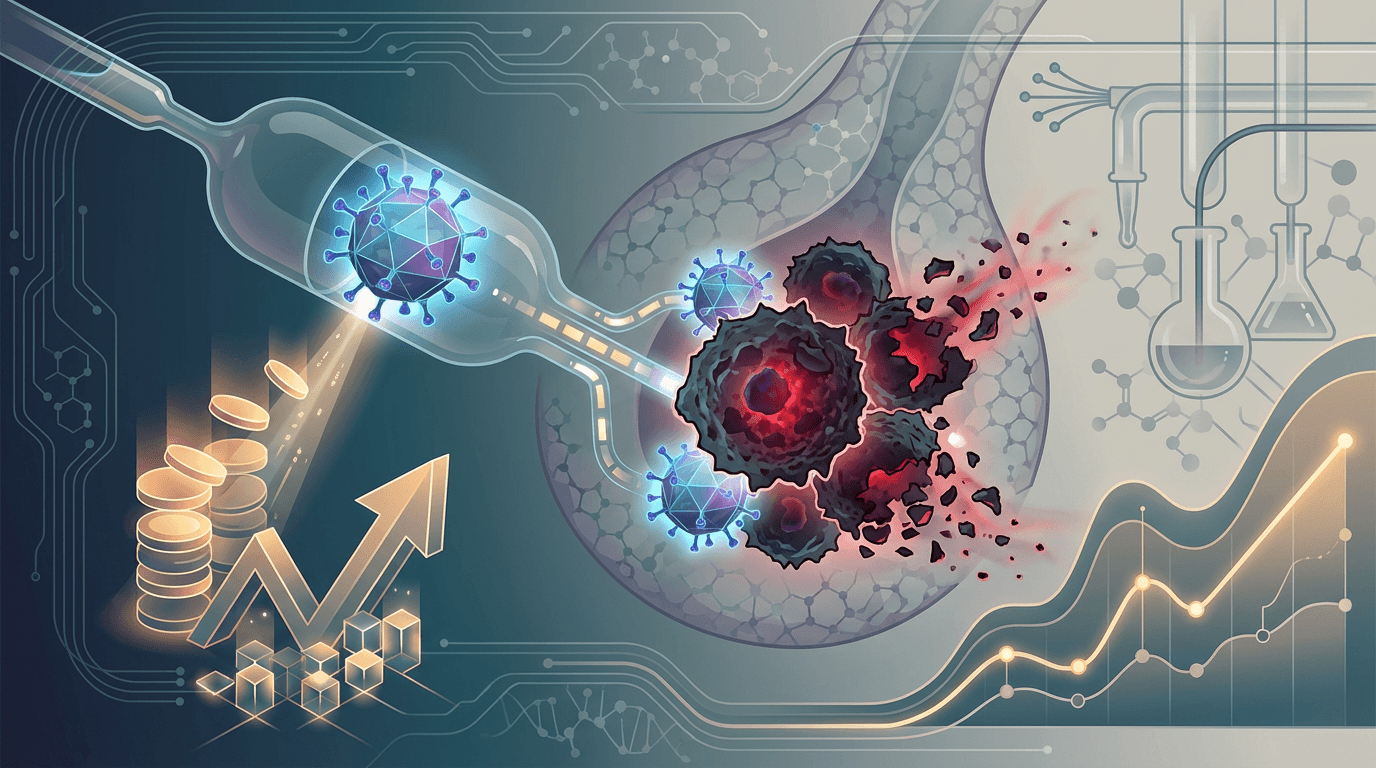

A Virus That Kills Prostate Cancer Just Got a $100M Backer

RTW Investments just agreed to hand Candel Therapeutics $100 million to launch a cancer-killing virus, but only if the FDA approves it first. The deal's clever structure and the Phase 3 data behind it could be a blueprint for small biotechs everywhere.

Most cancer drugs try to outsmart tumors with chemistry. Candel Therapeutics decided to fight biology with biology: by engineering a virus that infects cancer cells and teaches your immune system to destroy them. And now, a heavyweight investor just wrote a very large check to bet it works.

RTW Investments, a healthcare-focused fund, has agreed to hand Candel $100 million to launch its prostate cancer therapy CAN-2409 in the U.S. The catch? The money only arrives if the FDA approves the drug. It's a conditional bet, but one that says a lot about how confident RTW is in what Candel has built.

A Virus Walks Into a Tumor

Let's talk about what CAN-2409 actually does, because it's genuinely wild.

CAN-2409 is a genetically engineered adenovirus, the same family of viruses that cause the common cold. But this one has been reprogrammed. Doctors inject it directly into the prostate tumor, where it infects cancer cells and kills them. That's act one.

Act two is where it gets clever. When those cancer cells die, they spill their guts, releasing tumor-specific proteins that essentially wave a flag at your immune system. Think of it like a Most Wanted poster. Your immune cells learn what the cancer looks like and go hunting for it throughout the body. It's part virus, part vaccine, and entirely unlike traditional radiation or chemo.

Candel pairs the virus with a prodrug called valacyclovir, which amplifies the cancer-killing effect. The whole thing gets layered on top of standard radiation therapy. Patients aren't choosing between treatments; they're adding a biological weapon to their existing arsenal.

The Data That Got RTW's Attention

RTW didn't write this deal on vibes. The Phase 3 trial, called PrTK03, enrolled 745 patients with intermediate- to high-risk localized prostate cancer. Two-thirds got CAN-2409 plus standard radiation. The rest got a placebo plus the same radiation.

After a median follow-up of about 50 months, the results were clear: CAN-2409 patients saw a 30% reduction in the risk of recurrence or death compared to the control group. That translates to a 14.5% relative improvement in disease-free survival, meaning the cancer stayed gone longer in the patients who got the virus.

Get tomorrow's biotech intelligence before your competitors.

Join thousands of biotech professionals who start their day with our free, daily briefing.

Dig a little deeper and the data gets even more interesting. At the two-year biopsy mark, 80% of CAN-2409 patients showed a complete pathological response, meaning no detectable cancer. In the control group, that number was 64%. For prostate cancer-specific survival (stripping out deaths from other causes), the improvement jumped to roughly 38%-40%.

And the safety profile? Almost boring, in the best way. Serious treatment-related side effects hit just 1.7% of the CAN-2409 group, compared to 2.2% in the placebo arm. The most common complaints were mild flu-like symptoms, fever, and chills. You'd get worse from an actual cold.

This was the first multicenter Phase 3 trial in localized prostate cancer in over 20 years to hit both its primary and key secondary endpoints. That's not just a win for Candel; it's a milestone for the entire field.

The Deal: Smart Money, No Dilution

Now, here's where the business gets interesting, and where small biotechs everywhere should be taking notes.

Most small companies in Candel's position face an ugly choice when it comes to funding a drug launch: They can sell more stock (diluting existing shareholders) or take on debt (risking bankruptcy if sales start slow). Royalty financing offers a third path, and Candel just walked through it.

Under the deal, RTW pays Candel $100 million upon FDA approval. In return, RTW gets a tiered royalty on U.S. net sales: 4.67% on the first $1 billion in annual sales, dropping to just 1.33% above that. There's a built-in stick, too: if Candel misses certain sales thresholds, the lower-tier rate ratchets up to 6.67%. But the whole arrangement caps out once RTW collects $250 million total. After that, the royalty disappears.

It's basically a revenue-share deal with a ceiling. Candel gets launch cash without giving up equity. RTW gets a shot at a 2.5x return on a drug they believe in, and shareholders don't get crushed in the process.

RTW Managing Partner Roderick Wong, M.D., put it simply, saying the deal "reflects our confidence in Candel and the strong commercial potential of this therapy." Candel CEO Paul Peter Tak echoed that, calling it a chance to invest in a "world class commercial program" after approval.

How This Stacks Up

Candel's deal isn't happening in a vacuum. Royalty financing has been gaining steam across biotech as companies look for ways to fund launches without wrecking their cap tables.

For comparison, Royalty Pharma struck a $275 million deal with Denali Therapeutics in December 2025 for a Hunter syndrome therapy, but that came with a steeper 9.25% royalty on worldwide sales. Candel's terms are friendlier, with lower royalty rates and a U.S.-only scope, though the total deal size is smaller.

The conditional structure is the real tell. RTW doesn't pay a dime unless the FDA says yes. That means they've looked at the Phase 3 data, the safety profile, and the regulatory landscape, and decided the odds are in Candel's favor. It's not a guarantee, but it's a strong signal from people who do this for a living.

The Road Ahead

Candel plans to file its application with the FDA, called a BLA, or Biologics License Application, in Q4 2026. If approved, the $100 million from RTW flows in, and the commercial machine turns on.

The company isn't relying solely on this deal, either. Candel had $87 million in cash as of September 2025, plus a $130 million loan facility (with $50 million already drawn) and a planned $100 million public stock offering. That's a multi-layered financing strategy designed to get CAN-2409 across the finish line regardless of any single funding source.

Beyond prostate cancer, Candel has its virus platform working on non-small cell lung cancer and has a separate candidate called CAN-3110 in development for glioblastoma. But prostate cancer is the front of the line, and for good reason.

Why This Matters Beyond Candel

The oncolytic virus field has been a "someday" story for decades. The only approved oncolytic virus in the U.S. is IMLYGIC, a melanoma treatment that launched back in 2015. Japan approved one for brain cancer. But broadly, the technology has struggled to cross the gap from promising science to approved medicine.

CAN-2409's Phase 3 success could change the narrative. A clean win in a large, well-controlled trial, in a cancer that affects roughly 1 in 8 men, isn't easy to ignore. If the FDA agrees, it would be a landmark for the entire class of engineered-virus therapies.

And for small biotechs watching from the sidelines? Candel just showed there's a way to fund a launch without selling your soul, or your shares. RTW showed there's smart money willing to bet on good data, even when the check doesn't clear until the FDA says so.

Sometimes the best deals are the ones where both sides only win if the science works.

Science and Discovery

5 min read

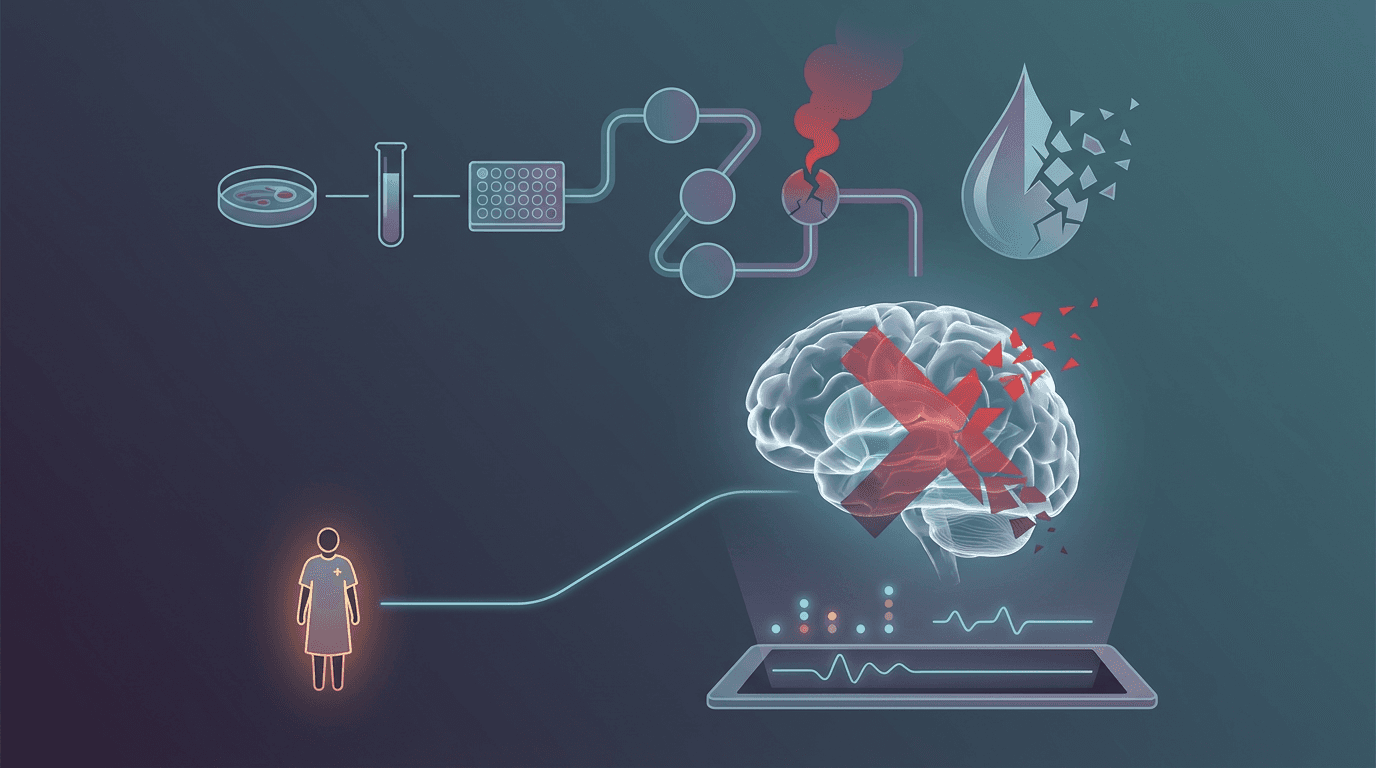

One Patient. That's All It Took to Kill This Alzheimer's Trial.

Ionis pulled the plug on an Alzheimer's trial for people with Down syndrome after enrolling just one patient in 14 months. The drug wasn't the problem; the brutal reality of rare disease recruitment was.